Markets do remain overvalued across the investment part

of the economy and we may see normalisation in some of

these segments.

We remain bullish on equities from a

medium to long term perspective.

Investors are suggested to have their asset

allocation plan based on one's risk appetite and

future goals in life.

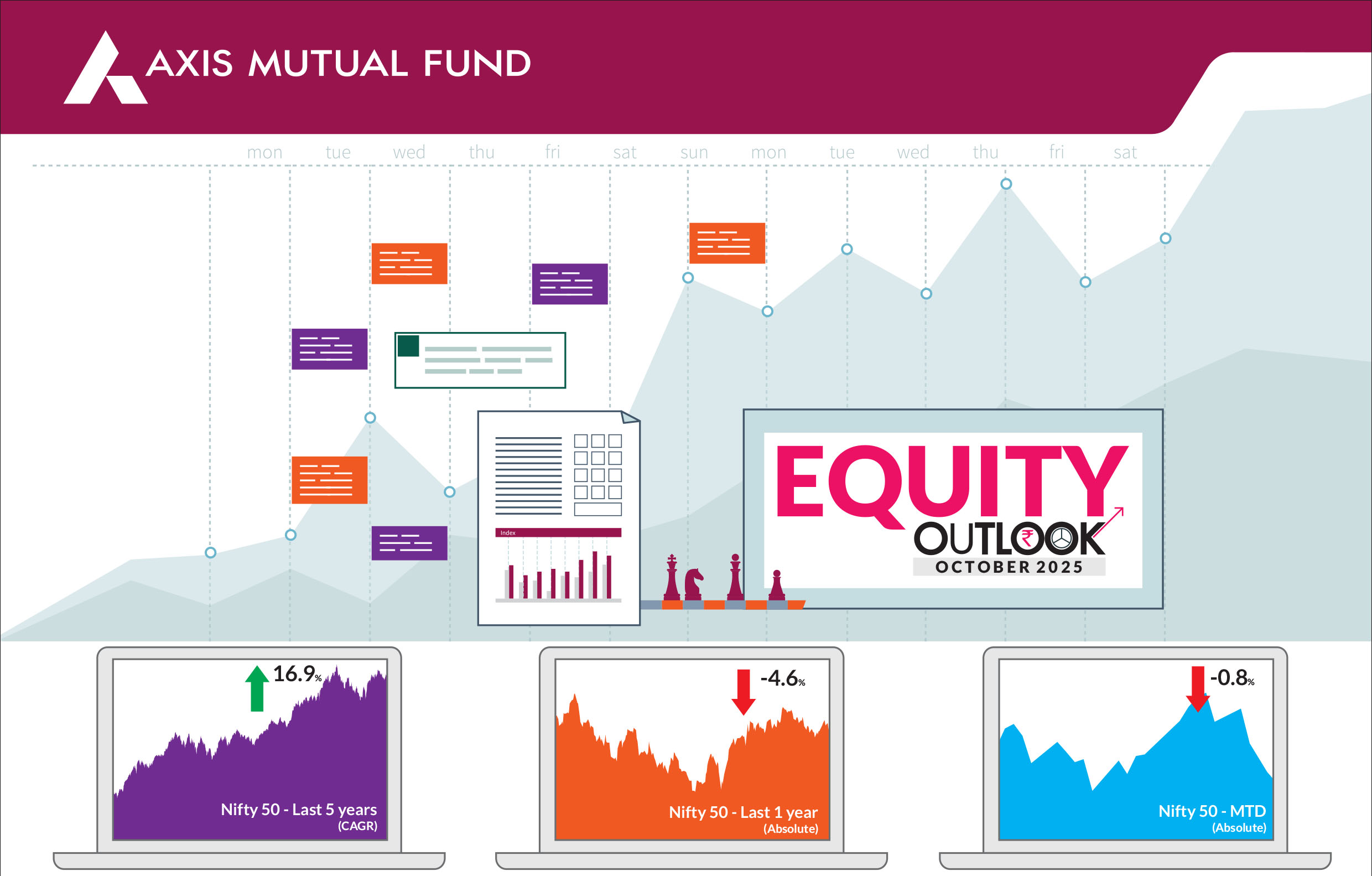

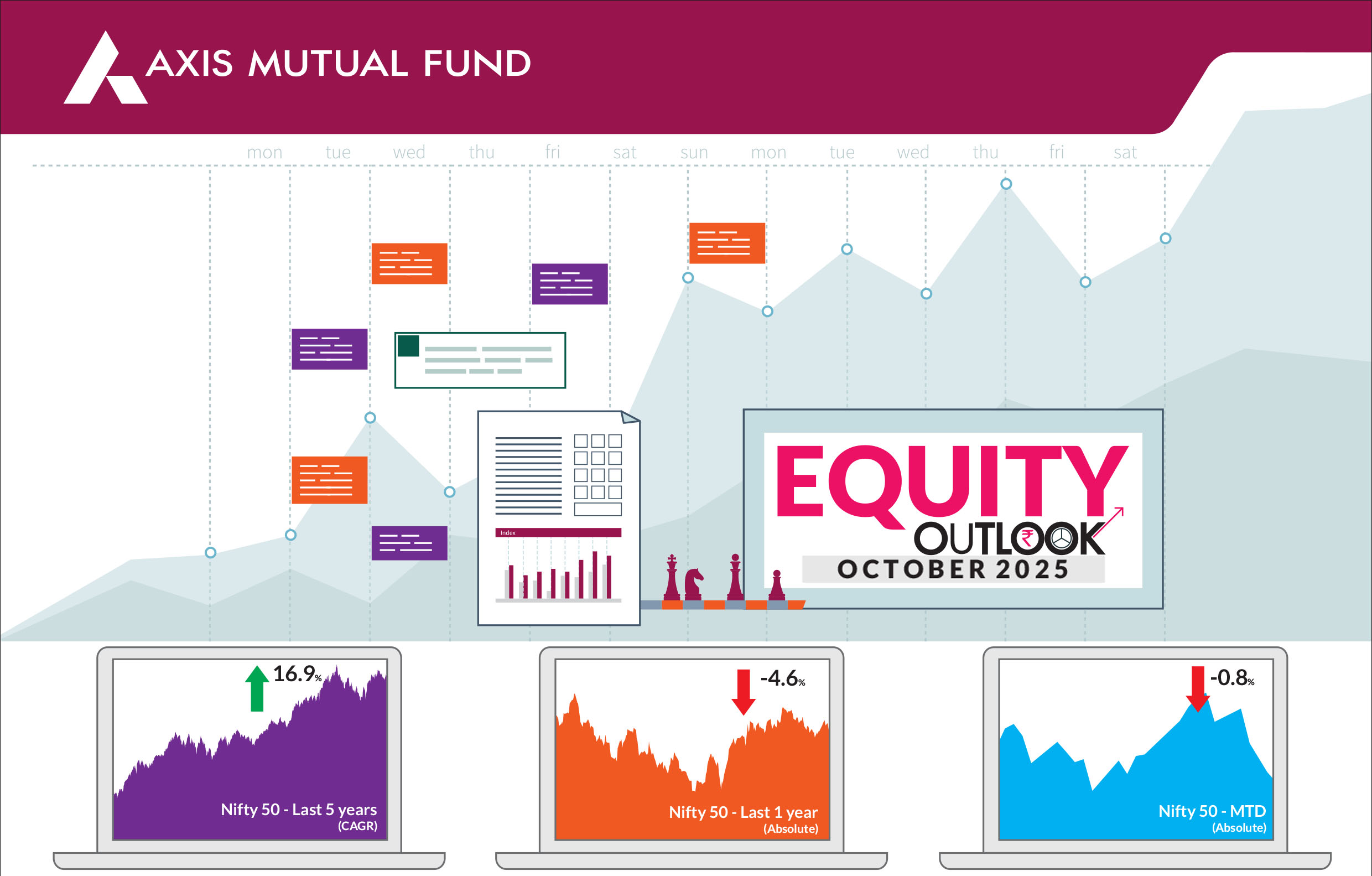

Indian equities started the month on a strong note amid positive news on GST rationalization, strong economic momentum and a 25 bps rate cut by the US Federal Reserve. However, this momentum was disrupted by a sharp market decline following the US administration's announcement of a one-time fee of US$100,000 on new H-1B visa petitions and a 100% tariff on branded drug imports. Consequently, the BSE Sensex and Nifty 50 ended the month with small gains of 0.6% and 0.8%, respectively. The mid and small-cap indices outperformed, with the NSE Midcap 100 rising by 1.4% and NSE Smallcap 100 gaining by 1.9%. At a sector level, metals, auto and oil & gas indices ended higher while consumer durables, IT and FMCG indices declined. Meanwhile, Foreign Portfolio Investors (FPIs) remained net sellers for the third consecutive month in September, pulling out US$2.7bn while Domestic Institutional Investors (DIIs) remained supportive with US$7.4bn in equity purchases. Year to date, FPI outflows total US$18bn while the DIIs bought to the tune of US$66.7bn. |

Key highlights of the month Key actions by the US government : The stalemate on the reciprocal tariffs scenario continues and this uncertainty has led to a dampened market sentiment. The additional measures initiated by the US such as a sharp increase in the H1B visa fees ands the import duty on branded drugs further impacted markets sentiment. India's pharmaceutical exports, being predominantly generic, are expected to face limited immediate impact from recent US trade measures. However, over time, these changes could influence procurement strategies, pricing structures, and regulatory priorities. In the IT services sector, stricter H-1B visa regulations are anticipated to raise onsite delivery costs and restrict workforce mobility.GST rationalization bodes well for durables and autos : GST rationalization is expected to gradually stimulate demand, with the auto sector already showing early signs of recovery ahead of the festive season. This positive momentum is likely to extend to other segments such as FMCG, consumer durables, cement, and broader discretionary categories, supported by rural recovery and recent direct tax relief measures. Additionally, the upcoming festive period is anticipated to further boost consumption across sectors, with rising expectations already evident in both the automobile and staples segments. |

Valuations off high, premium to EM falls : Given the rangebound movement in markets, valuations have come off the highs. On a relative basis, India’s premium to global and emerging markets is off higher levels. Such relative valuation premium levels of India to peers are nearly the lowest in four to five years. Yet, India remains one of the most expensive markets globally, only trailing the US. Outlook & Positioning Policy-driven catalysts could once again act as a turning point - the impact of GST reforms and the prospect of a favorable trade agreement with the US may serve as significant tailwinds in boosting economic activity including consumption.Against this backdrop, we continue to be overweight the consumption theme. If the macro tailwinds are effectively passed on to end consumers, they could reset India's consumption cycle. We are already seeing a high number of purchases in the discretionary segment such as automobiles and consumer durables. This also coincides with the festive season. We also remain constructive on other consumer discretionary plays-especially in retail, hospitality, and travel & tourism-which are poised to gain from strengthening domestic momentum and festive season demand. We have increased exposure to automobiles on the back of GST reforms and companies in this space have been quick to pass on the benefits to consumers. The trend toward premiumization is expected to strengthen, supported by a pickup in the replacement cycle. GST cuts are likely to reduce passenger vehicle (PV) prices by 5-10% and two-wheeler prices by around 8%, which should stimulate demand. We anticipate that aspirational product segments will benefit more due to higher demand elasticity. While improved affordability will encourage first-time buyers, we believe the revival in replacement demand-muted in recent years-will be a more significant growth driver for PVs. We are overweight NBFCs within financials as these are well-positioned to benefit from increased credit demand and improved liquidity conditions. Furthermore, we are overweight pharmaceuticals; the US tariff measures in pharma are directionally progressing with current US government stance suggesting little or no implication for generic companies with some negative implication for innovator or branded products companies. Overall, large US generic companies still face product concentration risk and subsiding tariff uncertainty though relative valuation are now approaching accommodative levels as the segment has lagged broader market. We remain underweight in IT. Additionally, we are positive on structural themes such as renewable capex, power transmission, and defense. Overall, India continues to offer a compelling medium- to long-term growth opportunity, supported by resilient domestic demand, a favorable rural outlook post-monsoon, and supportive macroeconomic indicators. |

Source: Bloomberg, Axis MF Research.